Start Your Summer With a Midyear Financial Checkup

Every December, there seems to be an endless number of articles imploring investors to conduct a year-end financial checkup. That’s not bad advice-but it comes at a time when many people are scrambling to deal with work and holiday responsibilities. That’s why you might consider doing a midyear financial review in place of-or along with-a […]

Fidato Wealth Recognized by Financial Advisor Magazine as a 2026 Top Investment Advisor

Fidato Wealth has yet again been named to Financial Advisor Magazine’s Top RIA Rankings, ranking #455 in the 2026 list of largest RIAs.

A Common Sense Guide to Heart Health

It’s been said that a man with health has a thousand dreams, while a man with no health has but one. Don’t you owe it to yourself, your family, your career and your community to have not only a thousand dreams, but also the energy and engagement to make them happen? Few would argue that, […]

Reclaim Your Time: Finding the Right Work-Life Balance

The “work first, life second” mantra guides far too many of us these days—from driven entrepreneurs to ladder-climbing professionals to overcommitted parents. One result: little to no time for family, friends, spouses, self-care, and other vital parts of living our best lives. If you are consistently putting work or volunteer projects at the top of […]

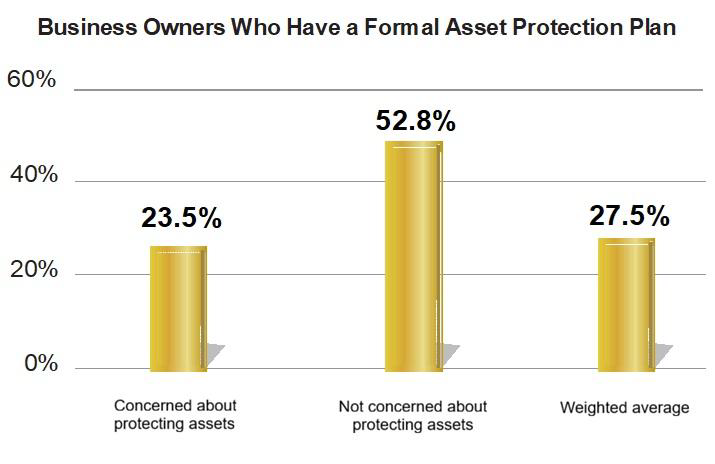

A Wall Around Your Wealth: The Importance of Asset Protection

Success can come with a major downside: It can make you a potential magnet for lawsuits—including frivolous and unfounded ones—and other attacks that can wreak havoc on your financial health and stability. Indeed, you may very well know someone in your life who has been sued. Maybe it was you! That means you’ve got to […]

Charitable Lead Trusts Can Help You To Help Many

If you’re like many investors, you may feel you’re in a kind of tug-of-war between two financial goals: 1) leaving money to your heirs and 2) benefiting organizations that are meaningful to you and that help people who need it. The good news: There are philanthropic tools that can potentially help you strike the right […]

Addressing Retirement’s Important Nonfinancial Challenges

Retirement is supposed to be idyllic, but it too often comes with social and emotional challenges. That’s likely always been the case, but it may be increasingly common. One possible reason: We’re living longer (in some cases, much longer) than past generations—which, in turn, allows more time for issues such as anxiety, depression and cognitive […]

Marissa Beyer Featured in The New York Times: How Strong Is Your Financial Knowledge? Take Our Quiz.

Fidato Wealth’s Marissa Beyer was featured in this article from the The New York Times, housing a quiz to help you test your Financial Knowledge.

Marissa Beyer Featured in Barron’s: It’s hard to manage relationships with divorcing couples. How these financial advisors do it.

Marissa Beyer discusses how to manage relationships with divorcing couples from a financial advisor’s position.

Women, Retirement and Longevity

Funding a comfortable retirement has the potential to be a challenging process for anyone. But women, in particular, are especially likely to confront a number of financial risks during their 60s, 70s and beyond. The main reason: Women have a well-established history of living longer than men as well as building less wealth than men […]